Financial Audits and Mechanisms for Good Governance of Public Funds

Author: Sammer Ahmad (CIA, CISA, CISM, SAP-FI) Director General (IT), SAI Pakistan

Good Governance of Public Funds

To finance government activities and provisions of public goods and services like healthcare, education, infrastructure, defense, and social welfare programs, public funds are used. These funds are usually managed by government entities and are subject to firm rules and oversight to ensure that they are used in most appropriate manner. Good governance, specifically with respect to public funds, discusses the principles and practices that ensure resources are managed appropriately, clearly, and in the best of public interest. Generally, good governance includes the following key principles:

- Accountability: Decision makers are responsible for their decisions and are accountable to the public representatives or other stakeholders;

- Transparency: Organizational decisions, actions and processes are open to scrutiny and review and are clearly communicated;

- Responsiveness: Processes and institutions produce products or services for the stakeholders within a reasonable time;

- Rule of law: Legal frameworks are applied fairly especially those related to human rights;

- Participation i.e. citizens have opportunity to participate in decision-making process either directly or indirectly;

- Equity and inclusiveness: All groups of people, most importantly, the poor have opportunities to progress or at least preserve their status; and finally,

- Efficiency and effectiveness: Products and services are produced in accordance with the needs of society with minimum cost and time.1

Good governance of public funds ensures service delivery, trust, and economic stability. It reduces waste, inhibits corruption, and assure that public funds provide benefits to the community as a whole.2 While pondering upon good governance of public funds, the United Nations Sustainable Development Goals (SDGs) can also be consulted, as they describe specific goals, relevant targets and their indicators for sustainable development. More specifically, good health and wellbeing, quality education, gender equality, climate finance, and reduced inequalities are more pertinent SDGs for consideration while spending public funds.3

Financial Audits

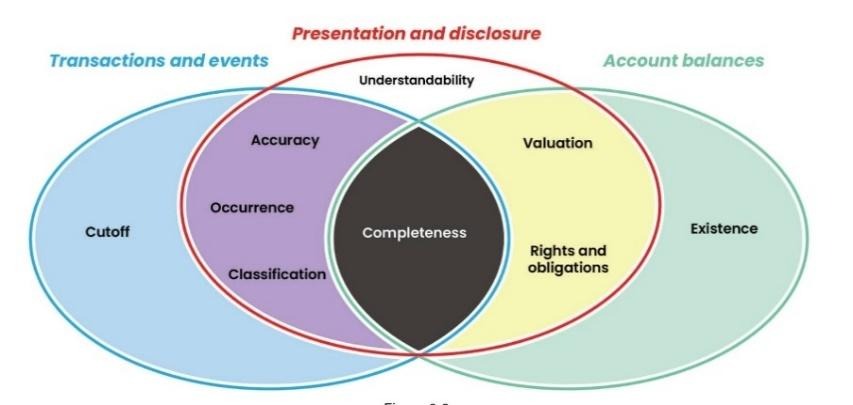

Financial audits revolve around assessing the validity of management’s assertions. These assertions are trifurcated into these categories: (1) transactions and events; (2) presentation and disclosure; and (3) account balances. There are in total nine types of assertions in all three categories, but ’Completeness’ is the only assertion that is common to all. Categories and their respective types of assertions are depicted here.4

Financial audit (sometimes called financial attest audit or certification audit) reviews and assesses the financial statements of an organization with respect to all of the above shown nine assertions. The balance sheet, statement of cash flows, profit and loss account, and notes to financial statements are reviewed and assessed against these assertions. While conducting the financial audit of expenditure of public funds, auditors evaluated whether the financial transactions are accurate, and the transactions happened due to occurrence of some past events. Moreover, whether the transactions are classified, completed, and within the cutoff date. Similarly, the financial auditors comment upon the remaining two categories and their respective and overlapped assertions. Finally, an opinion (unqualified, qualified, adverse or disclaimer of opinion) is given on the financial statements as a whole.

Internal Audits

Auditing plays a crucial role in combating corruption by improving transparency, accountability, and compliance with laws, rules and regulations. External audit provides independent financial assurance of organizations to identify any inconsistencies that could lead to corrupt or fraudulent practices. On the other hand, mechanisms used by internal auditing include detection and prevention. Internal audit function helps to identify non-compliance with laws, rules and regulations. Moreover, it detects red flags and suspicious transactions in the financial statements, records and data. In risk assessment and internal control mechanisms, auditors evaluate the design and effectiveness of internal controls, ensuring that safety measures against corrupt practices are in place. Compliance monitoring, whistleblowing, promoting ethical culture are other mechanisms that fall under the domain of internal auditing.

Requirements for Effective Audits

Before the start of any audit, including financial audit, auditors must align with certain attributes and characteristics as outlined in the ‘Lima Declaration’, otherwise known as the codes of ethics. These codes of ethics include integrity; trust, confidence, and credibility; independence, objectivity and impartiality; political neutrality; professional secrecy; competence; avoidance of conflict of interest; and professional development. After fulfilling the requirements of code of ethics, auditors must follow the second essential requirement of following the INTOSAI auditing standards for performing the audit. These standards include basic principles, general standards, field standards, and reporting standards. The INTOSAI standards are used in performing the audit cycle for the financial audit and is summarized below.5

- Audit Planning

- Establish audit objectives and scope.

- Understand the entity’s business.

- Assess materiality, planned precision, and audit risk.

- Understand the entity’s internal control structure.

- Determine components.

- Determine financial audit and compliance with authority objectives and error/irregularity conditions.

- Assess inherent and control risk.

- Determine test of internal control, analytical procedures and substantive tests of details.

- Activity and Resource Planning

- Develop audit program.

- Establish resource requirements and timing.

- Field Work

- Execute audit program.

- Evaluation

- Conclude audit work.

- Reporting

- Issue report.

- Follow-up

- Follow-up matters in reports.

Other mechanisms for ensuring good governance of public funds

Good governance of public funds leads to better decision making, efficient utilization of public resources, and stronger accountability processes for the administration of those resources. Ensuring transparency and accountability in the allocation of government funds and expenditure requires a mechanism that combines institutional structure, legal framework, and best oversight practices. For that purpose, below mentioned frameworks and mechanisms are widely used.

- Public financial management (PFM) framework:

This is the primary system for managing public funds and it includes, among others, budget formulation (i.e. planning and prioritization); budget implementation (i.e. spending the public money in accordance with the plan); and monitoring and evaluation (i.e. pursuing outcomes and impacts).

- Legislative oversight:

A parliamentary committee (e.g. Public Accounts Committee) reviews various audit reports and holds the respective public officials accountable. Laws may require prior parliamentary approval for various types of spending from public funds.

- Supreme Audit Institutions (SAIs):

The SAI (i.e. Office of the Auditor General) conducts audits of government spending and conveys the findings to the public representatives. Typical types of audit performed by the Office of Auditor General include financial attest, compliance with authority, and performance audits.

- Anti-corruption agencies:

These are the agencies with specialized mandates to investigate misappropriation and abuse of public funds and carry out anti-corruption laws. In Pakistan, at the federal level, there two organizations which deal with the corruption and money laundering— the Federal Investigating Agency (FIA) and the National Accountability Bureau (NAB). At the provincial level, there are anti-corruption departments.

- Procurement systems and e-procurement:

Procurement laws and digital procurement applications help hinder favoritism and fraud. Open bidding and information to the public regarding contract awards promote fairness and transparency in spending of public funds.

- Financial management information systems:

These automated systems tracks the flow of funds from allocation to expenditure in almost real time. They are very helpful for tracing and vouching financial transactions, allowing for easier assessment, validation, and verification of asset amounts in financial records.

- Legal and regulatory frameworks:

Laws related to public finance, regulations associated with procurements, and statutes pertaining to anticorruption serve as the basis of accountability. These laws, regulations, and statutes define the penalties for misuse of public funds and define the redress.

- Civil society and media oversight:

Non-governmental organizations and media help to monitor government spending to expose issues related to transparency. Investigative journalism can discover misappropriation of public funds.

- Citizen participatory audit:

This is a new form of auditing in which citizens participate in identifying findings while performing the audit. Citizens can take part in audit of government spending on services and projects by sharing useful, qualified, and well-supported information about the delivery of the services.

Conclusion and Recommendations

While performing any activity, there is always a risk of non-realization of activity’s objectives. To mitigate the risk, decision-makers should implement control mechanisms to manage the risk within an acceptable level. For instance, spending public funds for betterment of the people may fail in reaching its objectives. To mitigate this risk of failure, financial audits and other mechanisms presented above serve as control mechanisms. However, all control mechanisms have inherent limitations, such as collusion among employees and/or stakeholders; management override; and changing conditions. Decision-makers should focus on preventing and eliminating collusion among employees who deal with public funds. Moreover, a zero-tolerance policy should be adopted against management override. Furthermore, closely observing the changing socioeconomic conditions will help decision-makers respond appropriately and in a timely manner. Hence, good governance of public funds can be achieved, through tools like audits and other mechanisms, to support the well-being of the general public.

Bibliography

- CIA Gleim Material, 2023 edition.

- Financial Audit Manual, SAI Pakistan.

- Sawyer’s Internal Auditing, 7th Edition (2019).

- The Gardeners of Governance A Call to Action For Effective Internal Auditing by Rainer Lenz and Barrie Enslin, 2025.

- United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP).

- United Nations SDGs.

- United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP). ↩︎

- Ibid ↩︎

- SDGs of the United Nations. ↩︎

- CIA, Gleim study material 2023. ↩︎

- Financial Audit Manual, SAI Pakistan. ↩︎